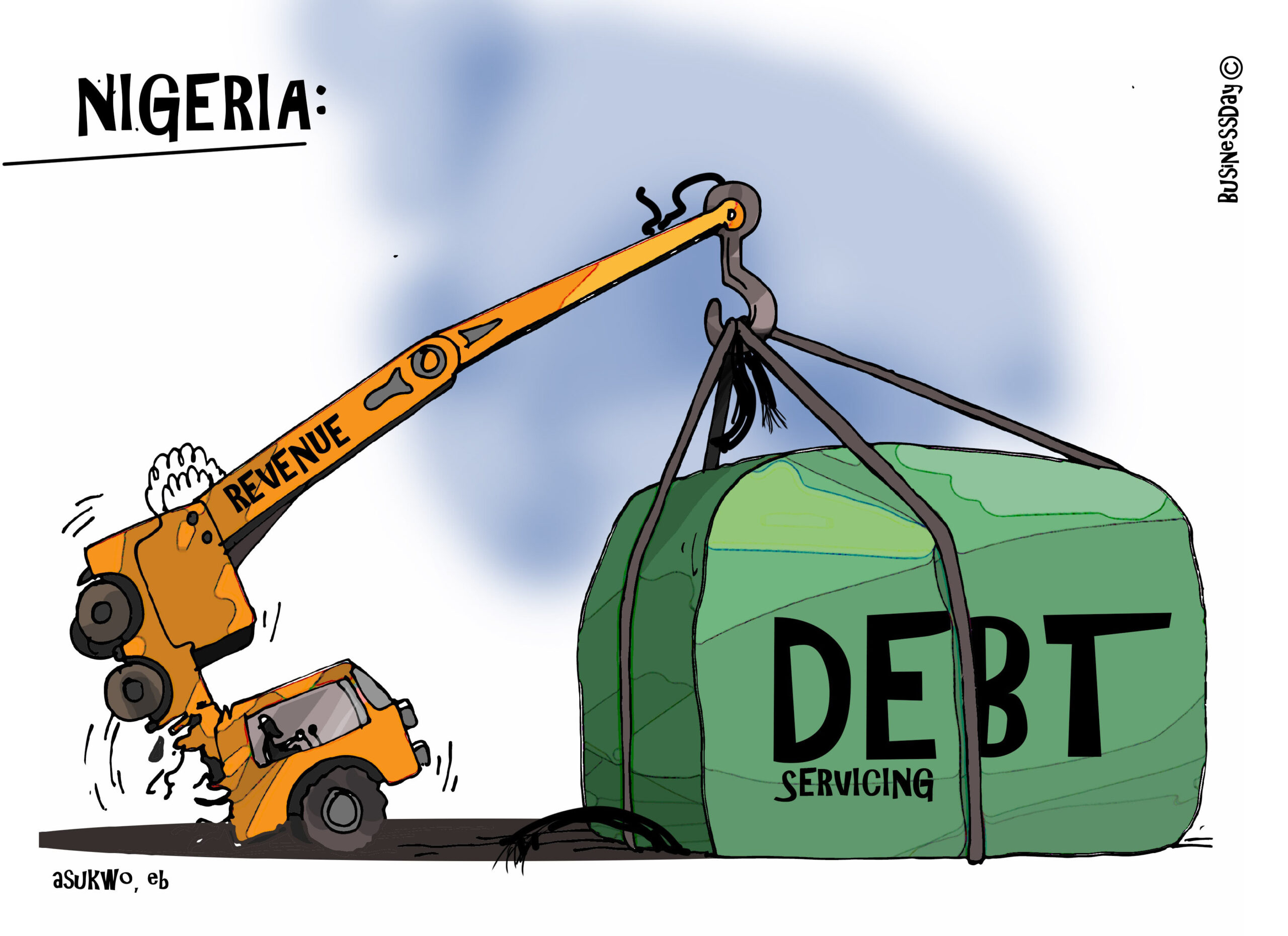

Nigeria is grappling with a familiar fiscal trap, where borrowing becomes the default solution when revenues fall short and reforms are politically inconvenient. The nation's debt servicing obligations are projected to reach a staggering $11.6 billion in the 2026 budget, a figure that has drawn sharp criticism and concern from various stakeholders.

According to BudgIT, Nigeria's debt service-to-revenue ratio has surged beyond 80 percent, a threshold significantly higher than globally accepted standards. This means a substantial portion of government earnings is allocated to debt repayment, leaving limited funds for critical development areas such as infrastructure, healthcare, and education.

The country's public debt has seen a dramatic increase, escalating from just over N33 trillion in 2021 to nearly N150 trillion in a few years. This rapid accumulation, dominated by domestic borrowing, is driving up interest rates and constricting credit availability for businesses, a phenomenon described as government borrowing crowding out the private sector.

Former Anambra State Governor, Peter Obi, has voiced strong concerns about the projected $11.6 billion debt servicing expenditure for 2026. He highlighted that while borrowing is not inherently problematic, its effectiveness hinges on productive investment and proper management, a contrast to Nigeria's current situation where a large portion of debt has not translated into visible developmental outcomes.

Obi pointed out that developed nations, despite high debt levels, channel borrowings into sectors like education, healthcare, and infrastructure, which generate long-term economic returns. He cited specific recent borrowings by Nigeria, including facilities from First Abu Dhabi Bank, UK Export Finance, and proposed World Bank and Deutsche Bank arrangements.

Meanwhile, the Debt Management Office (DMO) is actively managing the nation's debt through bond auctions. On May 18, 2026, Nigeria is auctioning N600 billion in reopened Federal Government bonds. These include a 10-year bond with a coupon rate of 22.60% due January 2035 and a 20-year bond with a coupon rate of 16.2499% due April 2037. The auction reflects the DMO's strategy of consolidating liquidity in existing bond lines amidst elevated interest rates.

The high yields on these bonds, particularly the 22.60% for the 10-year instrument, underscore the current high-rate borrowing environment. These FGN Bonds are designed to be attractive to institutional investors, qualifying for trustee investment, tax exemptions for pension funds, and serving as liquid assets for banks.

The persistent reliance on bond re-openings, as seen in multiple auctions since December 2025, indicates the Federal Government's significant dependence on domestic debt consolidation. This strategy, while providing necessary funding, raises questions about long-term fiscal sustainability and the potential burden on future generations if borrowing continues to finance consumption rather than productive investments.